Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Analyzing WEEX Exchange: Markets, Liquidity, and Transparency

Introduction

This report provides a comprehensive analysis of WEEX's trading environment, focusing on the following key areas:

Liquidity Depth: Assessment of market depth for major trading pairs on futures markets.

Asset Diversity: Evaluation of the variety and number of assets listed on the platform.

Comparative Analysis: Benchmarking WEEX against other leading cryptocurrency exchanges in terms of liquidity, asset offerings.

For the analysis of markets, we selected the 10 most actively traded coins and tokens. The assets are grouped into:

For the futures market, the analysis focuses on top-of-book liquidity (±0.1%), assessing the available volume at the best bid and ask prices. This approach provides a more accurate representation of immediate execution liquidity in the futures market. The data snapshot took place in May 2025.

Markets Analysis

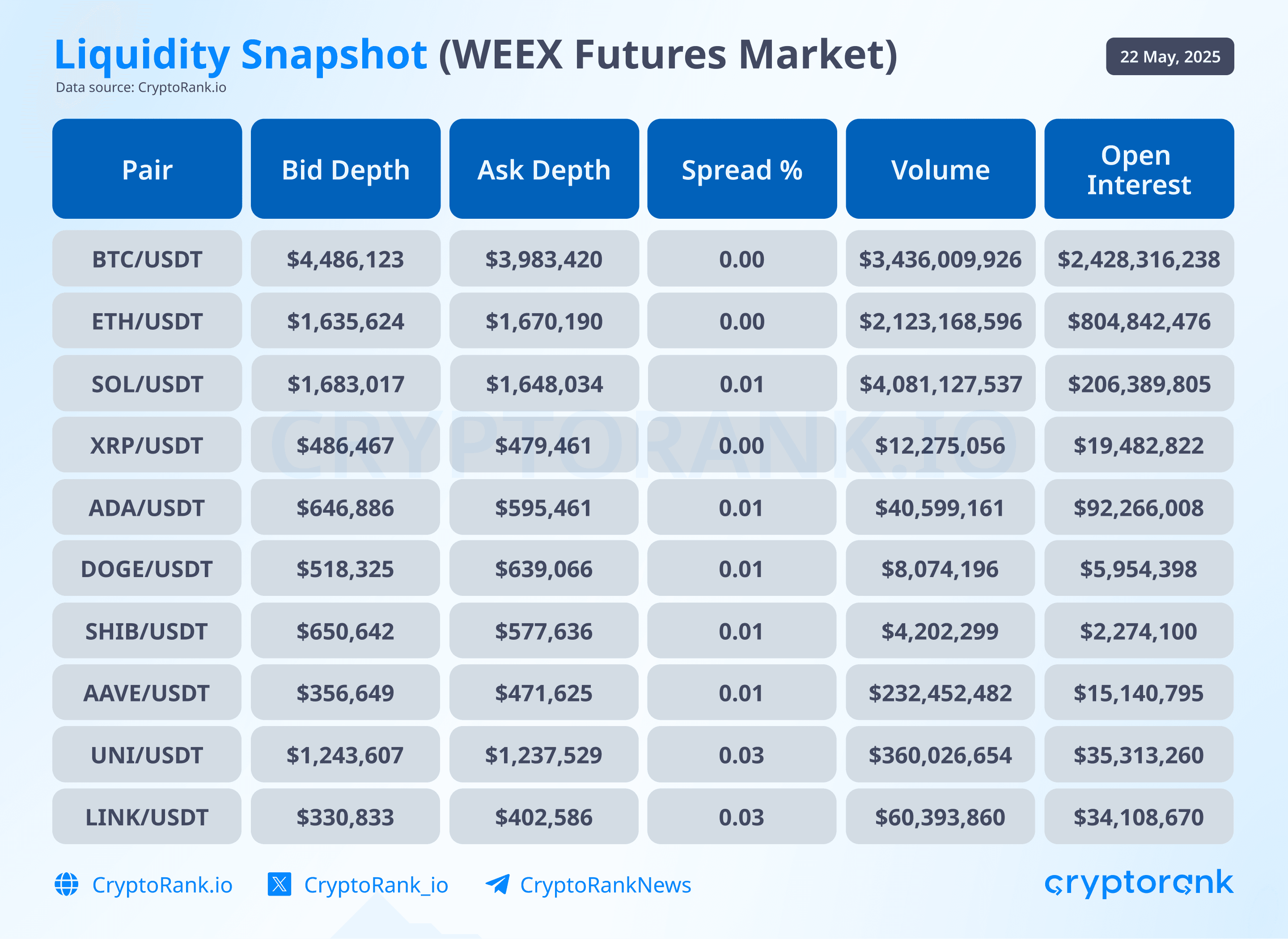

Liquidity Depth and Slippage Analysis on Futures Markets

WEEX’s futures markets demonstrate varied liquidity conditions across major and mid-cap assets. Using ±2% depth and spread as proxies for execution quality, the analysis reveals that only a handful of contracts exhibit deep enough order books to reliably handle large trades with minimal slippage.

BTC/USDT remains the most liquid futures pair, with a +2% depth of $4.49M and -2% depth of $3.98M, and a zero spread, which is ideal for large and frequent execution. ETH/USDT also shows solid liquidity, with approximately $1.6M on each side of the book, offering high availability for both retail and institutional traders. SOL/USDT performs similarly, maintaining tight spreads and order book depth exceeding $1.6M, indicating an active derivatives market.

UNI/USDT stands out with depth over $1.2M on each side and a moderate spread of 0.03%, suggesting stable market-making activity. Other pairs like DOGE/USDT, ADA/USDT, and SHIB/USDT maintain depth between $500k and $650k, with spreads holding around 0.01%, making them viable for moderate trading volume but vulnerable to slippage on larger orders.

Contracts such as AAVE/USDT, LINK/USDT, and XRP/USDT display more limited depth, ranging from $330k to $486k, with higher spreads (0.03% for LINK and UNI). These markets are better suited for smaller trades, as larger orders may lead to visible price movement.

Analyzing the Open Interest (OI) relative to trading volume, pairs like BTC/USDT and ETH/USDT indicate a healthy balance, suggesting sustainable liquidity and moderate speculative activity. XRP/USDT's high OI compared to its lower volume points to increased speculative positioning, possibly raising volatility risks.

Overall, WEEX provides high execution quality for top-traded assets like BTC, ETH, and SOL, while offering access to a wide range of altcoin derivatives with moderate to low liquidity. Traders should account for depth limitations and spread sensitivity when planning trade size and strategy across less liquid pairs.

Number of Listed Assets and Presence of Long-tail or Early-listed Tokens.

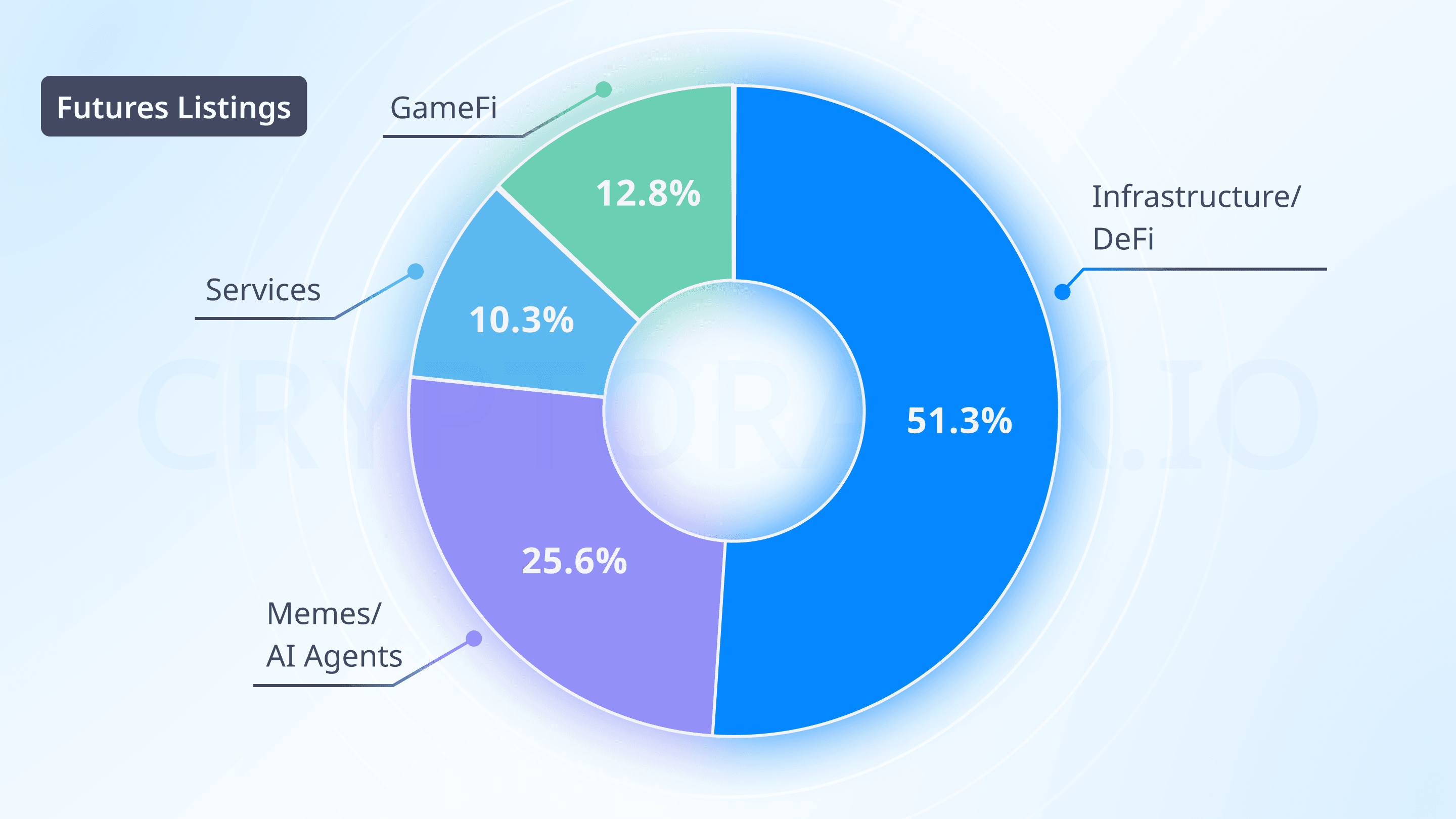

The number of futures trading pairs on WEEX exceeds 700. This highlights the dynamic nature of WEEX's futures offerings, which may appeal to traders seeking diverse derivative instruments. In the last month, WEEX introduced 39 new futures trading pairs.

The futures market prioritizes infrastructure and DeFi tokens (51.3% of new pairs), suggesting a focus on assets with stronger fundamentals or market stability, suitable for leveraged trading. The lower proportion of meme and AI agent tokens (25.6%) in futures indicates a more selective approach, likely to ensure liquidity and reduce risk in derivatives. The presence of GameFi (12.8%) and service-oriented tokens (10.3%) in futures further diversifies offerings, tapping into emerging trends like blockchain gaming.

The high volume of new listings (39 futures pairs in one month) underscores WEEX’s agility in responding to market trends. The emphasis on long-tail tokens in the spot market and early-listed projects across both markets, supported by the WE-Launch program, positions WEEX as a platform for discovering undervalued or emerging assets, appealing to a broad spectrum of traders.

WEEX demonstrates a notable presence of long-tail and early-listed tokens, enhancing its appeal for niche and emerging market traders. Long-tail tokens, defined as less popular or niche cryptocurrencies, are evident from recent listings on WEEX's new token announcements page, such as PUSSFi (PUSS), FARTGIRL, and 42069COIN, listed in April 2025. These tokens, often meme coins or projects with smaller market caps, are typically not widely traded on major exchanges, fitting the long-tail category.

Early-listed tokens, those listed shortly after launch, are supported through WEEX's WE-Launch program, which focuses on airdrops for early-stage crypto projects. The WE-Launch page details historical projects. The program's structure, requiring WXT staking for airdrops, further underscores WEEX's strategy to engage with emerging projects, likely attracting traders interested in growth opportunities.

In summary, WEEX lists around 700 for futures trading, with potential updates suggesting higher futures figures. The exchange actively supports long-tail and early-listed tokens, as evidenced by recent listings and the WE-Launch program, catering to a broad spectrum of trading preferences.

Comparison with Other Exchanges

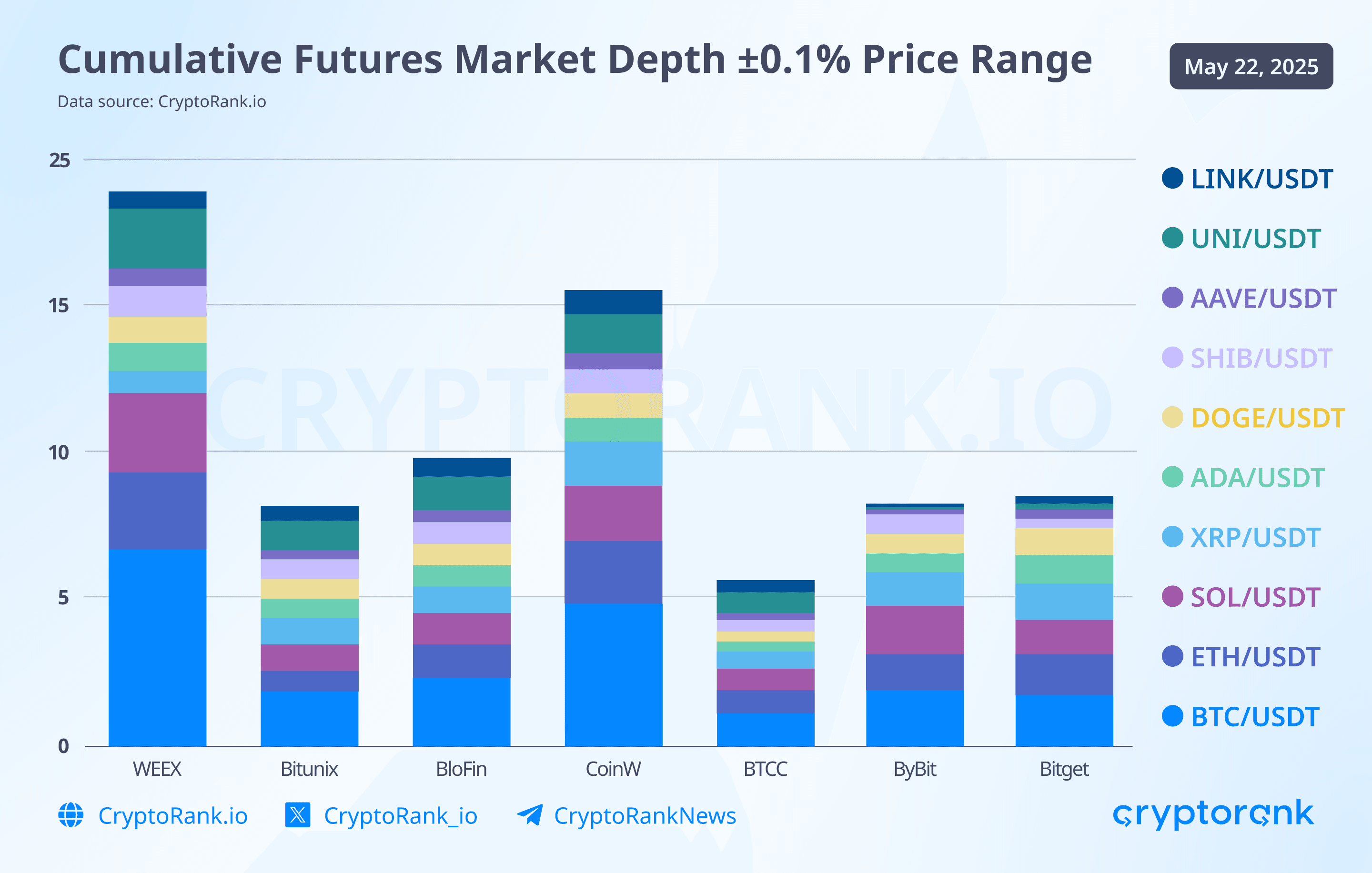

When WEEX is evaluated against other cryptocurrency exchanges, such as Bitunix, CoinW, BloFin, BTCC, Bybit, Bitget, in futures markets, several distinct patterns emerge regarding liquidity depth, execution quality, and asset coverage.

In the futures segment, WEEX offers more than 700 contracts, the largest among the compared platforms. This includes not only high-cap assets but also speculative tokens, AI-themed coins, and meme derivatives. Most competitors support 300–550 pairs, placing WEEX ahead in market exposure and product variety.

WEEX shows strong immediate liquidity on major trading pairs. For the BTC/USDT pair, WEEX offers the highest among all analyzed exchanges at the top of the book, surpassing both institutional platforms like Bitget and Bybit. Similar trends are observed for ETH/USDT and SOL/USDT well above top-of-book levels at competitors such as Bitunix, BloFin, and BTCC.

Bitget and Bybit show relatively low top-of-book volume, These platforms maintain a dense layer of small, rapidly replenished limit orders close to the mid-price. While this enables high-frequency trading and nearly instant execution for small orders, it means actual top-of-book depth appears limited in snapshots, even though liquidity increases significantly at slightly deeper levels such as within 0.1% of the mid-price. At these depths, WEEX and other mid-tier exchanges currently cannot compete with the scale and algorithmic liquidity density of Bybit and Bitget.

Liquidity on futures for pairs like SOL/USDT, ETH/USDT, and DOGE/USDT is sufficient for moderate volume trading. Notably, spreads on WEEX remain exceptionally low (0.00–0.01%), even on mid- and low-cap contracts, offering reliable execution conditions.

While it does not yet match the institutional-level liquidity of Bybit or Bitget on core futures pairs, WEEX remains highly competitive in spread efficiency and continues to build market depth. For traders focused on variety, early access, and efficient execution in liquid majors, WEEX represents a uniquely positioned alternative in the current exchange landscape.

Security and Transparency

WEEX maintains a strict 1:1 reserve ratio, ensuring that all user assets are fully backed. The platform provides a Proof of Reserves system, allowing users to verify that their holdings are matched by equivalent reserves. This system enhances trust and transparency by demonstrating the platform's solvency.

To safeguard user assets, WEEX has established a 1,000 BTC Protection Fund, serving as an emergency reserve to cover potential losses. The platform employs advanced security measures, including two-factor authentication (2FA), cold storage solutions, and regular security audits. WEEX has also undergone independent security assessments, affirming its commitment to maintaining high-security standards.

Conclusion

WEEX presents itself as a fast-evolving exchange with a strong balance between innovation, asset diversity, and user-focused infrastructure. WEEX demonstrates strengths that position it as a compelling alternative for retail and mid-size traders.

WEEX doesn’t yet match the institutional-grade depth and volume of the largest exchanges, but it competes effectively in fee efficiency, asset breadth, and execution quality on major pairs. Its aggressive listing approach and focus on emerging sectors give it an edge for users seeking fast access to new market opportunities.

For retail traders, WEEX offers an appealing mix of low fees, wide asset selection, and solid execution on leading pairs. Its support for long-tail tokens and early-stage projects makes it especially attractive to users following trends and new narratives in crypto.

In summary, WEEX is a well-rounded exchange for users who prioritize early access, cost efficiency, and diverse exposure, while accepting the trade-offs of moderate depth in less mainstream markets.

Join Us on the Next WEEX Adventure

This year, WEEX measured the world with our footsteps and earned trust through action. Whether you’re a trader, developer, or industry observer, we look forward to meeting you at our next stop.

Be Part of What’s Next! Register Now

Follow WEEX on social media:

· Instagram: @WEEX_Exchange

· X: @WEEX_Official

· Tiktok: @weex_global

· Youtube: @WEEX_Global

· Telegram: WeexGlobal Group

You may also like

From x402 to MPP: Cloudflare's crucial vote, will it go to Coinbase or Stripe?

BlackRock CEO issues annual open letter: The wave of tokenization has arrived, and we will lead this trend

When Backpack backstabs the community

When gold is no longer a safe haven, and Bitcoin continues to panic

Trump, the World's Largest Oil Trader

If the US and Iran have not reached an agreement in 5 days, what other cards does Trump have?

Tether Whale Dumps £12 Million, Backing Crypto’s ‘British Trump’

Ethereum Foundation Post: Rethinking the Division of Work Between L1 and L2 to Build the Ultimate Ethereum Ecosystem

Two Major Prediction Market Platforms Unite Rarely, What Is the Story Behind This New Fund?

Dragonfly Partners: Most agents will not engage in autonomous trading, how can crypto payments prevail?

US AI Startup Goes All In on Chinese Mega-Model | Rewire News Morning Brief

Trump Lies Again: A "Five-Day Pause" Psyop, How Wall Street, Bitcoin, and Polymarket Insiders Synced Uposciogen

When a Token Becomes Labor, People Become the Interface

Ceasefire News Leaked Ahead of Time? Large Polymarket Bets on Outcome Before Trump's Tweet

BlackRock CEO's Annual Shareholder Letter: How is Wall Street Using AI to Keep Profiting from National Pension Funds?

Sun Valley Releases 2025 Financial Report: Bitcoin Mining Revenue Reaches $670 Million, Accelerating Transformation to AI Infrastructure Platform

On March 16, 2026, in Dallas, Texas, USA, CanGu Company (New York Stock Exchange code: CANG, hereinafter referred to as "CanGu" or the "Company") today announced its unaudited financial performance for the fourth quarter and full year ended December 31, 2025. As a btc-42">bitcoin mining enterprise relying on a globally operated layout and dedicated to building an integrated energy and AI computing power platform, CanGu is actively advancing its business transformation and infrastructure development.

• Financial Performance:

Total revenue for the full year 2025 was $688.1 million, with $179.5 million in the fourth quarter.

Bitcoin mining business revenue for the full year was $675.5 million, with $172.4 million in the fourth quarter.

Full-year adjusted EBITDA was $24.5 million, while the fourth quarter was -$156.3 million.

• Mining Operations and Costs:

A total of 6,594.6 bitcoins were mined throughout the year, averaging 18.07 bitcoins per day; of which 1,718.3 bitcoins were mined in the fourth quarter, averaging 18.68 bitcoins per day.

The average mining cost for the full year (excluding miner depreciation) was $79,707 per bitcoin, and for the fourth quarter, it was $84,552;

The all-in sustaining costs were $97,272 and $106,251 per bitcoin, respectively.

As of the end of December 2025, the company has cumulatively produced 7,528.4 bitcoins since entering the bitcoin mining business.

• Strategic Progress:

The company has completed the termination of the American Depositary Receipt (ADR) program and transitioned to a direct listing on the NYSE to enhance information transparency and align with its strategic direction, with a long-term goal of expanding its investor base.

CEO Paul Yu stated: "2025 marked the company's first full year as a bitcoin mining enterprise, characterized by rapid execution and structural reshaping. We completed a comprehensive adjustment of our asset system and established a globally distributed mining network. Additionally, the company introduced a new management team, further strengthening our capabilities and competitive advantage in the digital asset and energy infrastructure space. The completion of the NYSE direct listing and USD pricing also signifies our transformation into a global AI infrastructure company."

"As we enter 2026, the company will continue to optimize its balance sheet structure and enhance operational efficiency and cost resilience through adjustments to the miner portfolio. At the same time, we are advancing our strategic transformation into an AI infrastructure provider. Leveraging EcoHash, we will utilize our capabilities in scalable computing power and energy networks to provide cost-effective AI inference solutions. The relevant site transformations and product development are progressing simultaneously, and the company is well-positioned to sustain its execution in the new phase."

The company's Chief Financial Officer, Michael Zhang, stated: "By 2025, the company is expected to achieve significant revenue growth through its scaled mining operations. Despite recording a net loss of $452.8 million from ongoing operations, mainly due to one-time transformation costs and market-driven fair value adjustments, the company, from a financial perspective, will reduce its leverage, optimize its Bitcoin reserve strategy and liquidity management, introduce new capital to strengthen its financial position, and seize investment opportunities in high-potential areas such as AI infrastructure while navigating market volatility."

The total revenue for the fourth quarter was $1.795 billion. Of this, the Bitcoin mining business contributed $1.724 billion in revenue, generating 1,718.3 Bitcoins during the quarter. Revenue from the international automobile trading business was $4.8 million.

The total operating costs and expenses for the fourth quarter amounted to $4.56 billion, primarily attributed to expenses related to the Bitcoin mining business, as well as impairment of mining machines and fair value losses on Bitcoin collateral receivables.

This includes:

· Cost of Revenue (excluding depreciation): $1.553 billion

· Cost of Revenue (depreciation): $38.1 million

· Operating Expenses: $9.9 million (including related-party expenses of $1.1 million)

· Mining Machine Impairment Loss: $81.4 million

· Fair Value Loss on Bitcoin Collateral Receivables: $171.4 million

The operating loss for the fourth quarter was $276.6 million, a significant increase from a loss of $0.7 million in the same period of 2024, primarily due to the downward trend in Bitcoin prices.

The net loss from ongoing operations was $285 million, compared to a net profit of $2.4 million in the same period last year.

The adjusted EBITDA was -$156.3 million, compared to $2.4 million in the same period last year.

The total revenue for the full year was $6.881 billion. Of this, the revenue from the Bitcoin mining business was $6.755 billion, with a total output of 6,594.6 Bitcoins for the year. Revenue from the international automobile trading business was $9.8 million.

The total annual operating costs and expenses amount to $1.1 billion.

Specifically, they include:

· Revenue Cost (excluding depreciation): $543.3 million

· Revenue Cost (depreciation): $116.6 million

· Operating Expenses: $28.9 million (including related-party expenses of $1.1 million)

· Miner Impairment Loss: $338.3 million

· Bitcoin Collateral Receivable Fair Value Change Loss: $96.5 million

The full-year operating loss is $437.1 million. The continuing operations net loss is $452.8 million, while in 2024, there was a net profit of $4.8 million.

The 2025 non-GAAP adjusted net profit is $24.5 million (compared to $5.7 million in 2024). This measure does not include share-based compensation expenses; refer to "Use of Non-GAAP Financial Measures" for details.

As of December 31, 2025, the company's key assets and liabilities are as follows:

· Cash and Cash Equivalents: $41.2 million

· Bitcoin Collateral Receivable (Non-current, related party): $663.0 million

· Miner Net Value: $248.7 million

· Long-Term Debt (related party): $557.6 million

In February 2026, the company sold 4,451 bitcoins and repaid a portion of related-party long-term debt to reduce financial leverage and optimize the asset-liability structure.

As per the stock repurchase plan disclosed on March 13, 2025, as of December 31, 2025, the company had repurchased a total of 890,155 shares of Class A common stock for approximately $1.2 million.

The US AI Startup Is Loving China's Open Source Model