- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Breakdown of Coinbase 2024 Financial Report: Annual Revenue Doubles to Nearly $6.6 Billion, Q4 Achieves Highest Quarterly Revenue in Three Years

Source: CoinBase

Original Article Compilation: Felix, PANews

Coinbase announced its fourth-quarter and full-year earnings on February 13. Thanks to a strong post-election rebound that drove cryptocurrency prices to new highs at the end of last year, Coinbase's fourth-quarter performance exceeded expectations, achieving its largest quarterly revenue in three years.

Coinbase reported an earnings per share of $4.68, more than double the analysts' expectation of $2.11, with a fourth-quarter profit of $1.3 billion.

In after-hours trading, Coinbase's stock price rose 2% to around $304, with a 112% increase in stock price over the past year. This article provides a quick overview of key data in Coinbase's financial report.

2024 Full-Year Revenue Doubled, Q4 Contributed Over 30% of Revenue

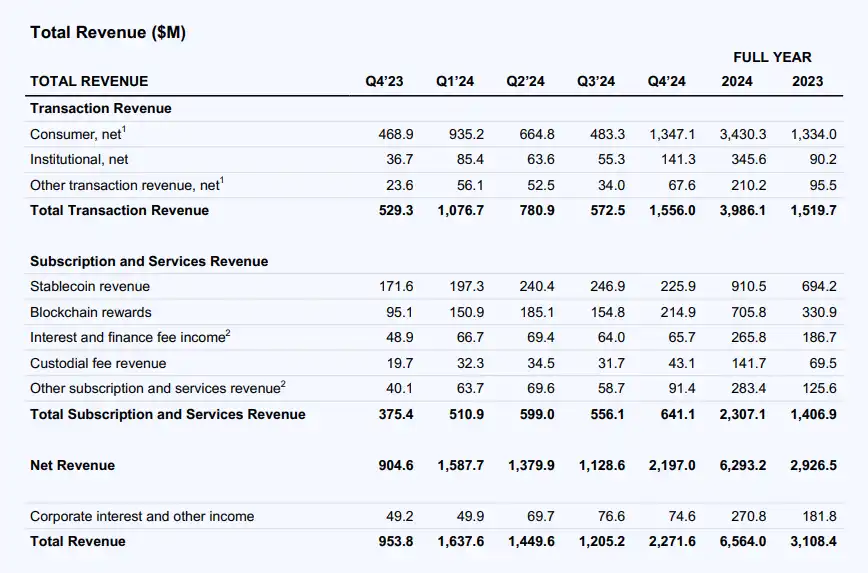

2024 was a strong year for cryptocurrency and Coinbase, with annual revenue more than doubling to $6.564 billion, net income of $2.6 billion, and adjusted EBITDA of $3.3 billion. In Q4, revenue reached $2.27 billion, an 88% increase from the previous quarter.

In terms of products, Coinbase gained market share in the U.S. spot and derivative trading products in 2024 and added custody, staking, and USDC assets to its product suite to drive revenue diversification. Additionally, Coinbase further promoted the adoption of products like Base, Coinbase One, Prime Financing, and international expansion.

Trading Revenue

Full-year 2024 trading revenue was $4 billion, a 162% year-over-year growth, with a total trading volume of $1.2 trillion, a 148% year-over-year increase. Retail trading volume was $221 billion, up 195% year-over-year, and institutional trading volume was $941.2 billion, up 139% year-over-year. In Q4, Coinbase's trading revenue reached $1.6 billion, a 172% increase from the previous quarter, with a trading volume of $439 billion, a 185% year-over-year increase.

The majority of Coinbase's year-over-year trading volume growth in 2024 was due to increased cryptocurrency asset volatility levels, especially in the first and fourth quarters, as well as the rise in average cryptocurrency prices. Two key factors supporting these stronger macroeconomic conditions were the launch of a Bitcoin ETF product in Q1 2024 and the election of a pro-cryptocurrency president and congress in Q4 2024, along with expectations of regulatory clarity, all of which led to increased spot cryptocurrency trading activity.

In addition, Coinbase increased its market share in the U.S. spot market in 2024. On the spot side, Coinbase added initial listing work (i.e., the first centralized exchange to list a token for trading and custody) and added 48 new spot trading assets.

Furthermore, Coinbase also successfully expanded its derivatives business in 2024. For example, it added 92 new assets for trading on the international exchanges. While still in the early stages, both retail and institutional derivative trading volumes and market share hit record highs in the fourth quarter.

Retail Trading Revenue

In the fourth quarter, retail trading volume was $940 billion, a 176% increase compared to the previous period, far surpassing the 126% increase in the U.S. spot market. This quarter's retail trading revenue was $1.3 billion, a 179% increase compared to the previous period. This may be related to Coinbase's addition of 13 new assets in the fourth quarter, including popular memecoins such as PEPE and WlF. Overall, these efforts (along with market conditions) drove MTU up 24% sequentially.

Institutional Trading Revenue

In the fourth quarter, institutional trading volume was $3.45 trillion, a 128% increase compared to the previous period, outperforming the U.S. spot market. This quarter's institutional trading revenue was $141 million, a 156% increase compared to the previous period. The fourth quarter showed strong performance, with revenue growth significantly outpacing that of exchanges and Primes. In addition to strong market conditions, the institutional business also demonstrated strong momentum.

Other Trading Revenue

In the fourth quarter, other trading revenue was $68 million, a 99% increase compared to the previous period, mainly driven by Base's sorter revenue increase. As a result of increased network demand and rising ETH prices in the fourth quarter, transaction volumes continued to grow sequentially, with higher revenue per transaction. The average cost per transaction remains below the target of $0.01.

Subscription and Services Revenue

In 2024, subscription and services revenue was $2.3 billion, a 64% year-over-year increase, about 4.5 times higher than the 2021 bull market level. Most of the year-over-year growth in 2024 came from blockchain rewards revenue, stablecoin revenue, and Coinbase One subscription revenue.

Subscription and Service Revenue in Q4 was $641 million, a 15% increase QoQ. Stablecoin revenue in Q4 decreased by 9% QoQ to $226 million, but grew by 31% YoY to $910 million for the full year. Overall, USDC was the fastest-growing "major" stablecoin in 2024. The driver of Q4 stablecoin revenue was the significant increase in the average market cap of USDC and the USDC assets in the product suite.

Blockchain Rewards Revenue in Q4 was $215 million, a 39% increase QoQ. The growth was driven by the rise in cryptocurrency asset prices, an increase in the average protocol reward rate (especially SOL), and continued inflows of native assets.

Interest and Financing Revenue in Q4 was $66 million, a 3% increase QoQ. The growth primarily came from the Prime Financing business, which saw a historic high in loan balances shortly after the U.S. election in early November. The growth in loan volume was driven by increased trade financing activity related to ETF products and higher utilization of bilateral loan products. The growth in Prime Financing fees was partially offset by a decline in revenue from customer custody fiat balances, as the average balance increased by 7% QoQ to $5.1 billion, but the actual interest rate decline offset this growth.

Custody Fees Revenue in Q4 was $43 million, a 36% increase QoQ. The growth was driven by the rise in cryptocurrency asset prices and the continued growth in custody volumes. BTC inflows were the primary driver of growth, benefiting from Coinbase's role as the primary custodian for the vast majority of ETFs and other client activities. Additionally, it benefited from the Fourth Quarter New Asset Launch program. As of Q4, Assets Under Custody ("AUC") were $220 billion, which is a part of the platform's total assets.

Other Subscription and Service Revenue was $91 million, a 56% increase QoQ. Coinbase One was the biggest driver of the QoQ growth.

Annual Operating Expenses at $4.3 billion, Trading and Marketing Costs Increase

2024 total operating expenses were $4.3 billion, a 30% increase YoY to $1 billion. Technology & Development, General & Administrative, and Sales & Marketing expenses totaled $692 million, a 25% YoY increase. The growth was primarily driven by an increase in variable area expenses, especially USDC reward expenses and marketing costs, and higher stock-based compensation and policy expenses as the cryptocurrency outreach intensified. The year ended with 3,772 full-time employees, a 10% YoY increase.

The total operating expenses in the fourth quarter were $1.2 billion, a 19% increase from the previous quarter to $202 million, primarily driven by an increase in transaction activity leading to higher transaction fees. Technology and development, general and administrative, and sales and marketing expenses collectively increased by $84 million, a 10% quarterly increase, mainly due to performance marketing expenses, increased USDC incentives (as a result of a significant increase in USDC assets in the product suite), and policy-related expenses.

The fourth-quarter transaction expenses were $317 million, representing 14% of net revenue, an 85% quarter-over-quarter increase. The sequential increase was primarily attributed to higher transaction volumes, blockchain reward costs, and blockchain transaction fees (mainly in BTC and ETH).

Technology and development expenses were $369 million, a 2% decrease from the previous quarter. The decrease was due to lower personnel-related costs, although an increase in professional service-related expenses partially offset this decrease.

General and administrative expenses totaled $363 million, a 10% increase from the previous quarter. The growth was driven by customer support investments, related to the robust market environment in the fourth quarter, increased legal expenses, and policy-related spending.

Sales and marketing expenses were $226 million, a 37% quarter-over-quarter increase. This increase supported the fourth quarter's market momentum through increased variable performance marketing expenses and promotional activities to drive user acquisition and revenue growth in the US and internationally. Due to the increased USDC assets in the product suite, USDC incentives also increased by 29% quarter-over-quarter, reaching $80 million.

Furthermore, in terms of share count, Coinbase had a fully diluted share count of 286.5 million shares at the end of the fourth quarter. This figure includes 253.6 million common shares and 32.9 million diluted shares.

In terms of capital and liquidity, as of the end of the fourth quarter, Coinbase had $9.3 billion in USD resources. USD resources are defined as cash and cash equivalents and USDC (excluding USD lent out as collateral or pledged). USD resources increased by 13% quarter-over-quarter to $1.1 billion.

Q1 2022 Has Achieved $750 Million in Transaction Revenue, Continuing to Drive Revenue Diversification

The report stated that as of February 11, Coinbase has generated approximately $750 million in transaction revenue in Q1 2022. Coinbase expressed efforts to achieve revenue diversification, no longer solely relying on trading. Based on last year's financial report, as of the fourth quarter, Coinbase's trading revenue accounted for 68.5% of its total revenue, with the majority coming from retail traders.

This quarter, revenue from its subscription and services business (including stablecoin, staking, custody, and Coinbase One products) is expected to be between $6.85 billion and $7.65 billion.

Coinbase also expects that the USDC stablecoin issued by Circle and covered by a revenue-sharing agreement with Coinbase will drive quarter-over-quarter growth in sales and marketing expenses in the first quarter.

Coinbase CEO Brian Armstrong stated during the earnings call that the company has a "grand vision for making USDC the first stablecoin."

The percentage of transaction fees as a share of net revenue is expected to reach a mid-to-high level. Technology and development as well as general and administrative expenses are expected to be between $7.5 billion and $8 billion. In addition, wage taxes are expected to increase seasonally quarter over quarter. The net profit growth rate is expected to be slightly higher than in the fourth quarter.

Sales and marketing expenses in the first quarter of 2025 are expected to be between $2.35 billion and $3.75 billion. Since the mid-fourth quarter, there has been a significant increase in marketing opportunities that meet or exceed the threshold for return on investment in both new and existing paid marketing channels in the U.S. and major international markets. Nonetheless, due to the ongoing volatility in the crypto market, there is significant daily variance in effectiveness marketing expenses in the first quarter. Therefore, the potential outcome range for the first quarter is much larger than in previous periods. Whether within this range will largely depend on

· continued attractive marketing opportunities in the remaining time of the first quarter, historically closely tied to market fluctuations and asset prices

· USDC assets in the product suite driving USDC rewards. As a reference, this represents approximately 35% of sales and marketing expenses in the fourth quarter

Original Source Link

You may also like

AI within artillery range

“The cloud” is a metaphor, but the data center isn’t.

March 4th Market Key Intelligence, How Much Did You Miss?

Taking Stock of Crypto's Washington Power Players: Who is Advocating for US Crypto Regulation?

DDC Enterprise Limited Announces 2025 Unaudited Preliminary Financial Performance: Record Revenue Achieved, Bitcoin Treasury Grows to 2183 Coins

On March 4, 2026, DDC Enterprise Limited (NYSE American: DDC) today announced preliminary, unaudited full-year financial performance for the year ended December 31, 2025. The company expects to achieve record revenue and record positive adjusted EBITDA, primarily driven by continued growth in its core consumer food business and overall margin improvement. The final audited financial report is expected to be released in mid-April 2026.

Revenue: Expected to be between $39 million and $41 million, reaching a new company high.

Organic Growth: Excluding the impact of the company's strategic contraction of its U.S. operations, core revenue is expected to grow 11% to 17% year over year.

Gross Profit Margin: Expected to be between 28% and 30%, reflecting continued operational efficiency improvements.

Adjusted EBITDA: The company expects to achieve a positive full-year result in 2025, a significant improvement from a $3.5 million loss in 2024, mainly due to rigorous cost controls and a higher-margin sales mix.

In 2025, DDC's core consumer food business maintained strong operational performance.

The company also disclosed Core Consumer Food Business Adjusted EBITDA, a metric that further excludes costs related to its Bitcoin reserve strategy and non-cash fair value adjustments related to its Bitcoin holdings from adjusted EBITDA to more accurately reflect the core business performance.

In 2025, Core Consumer Food Business Adjusted EBITDA is expected to be between $5.5 million and $6 million.

In the first half of 2025, DDC initiated a long-term Bitcoin accumulation strategy, holding Bitcoin as its primary reserve asset.

As of December 31, 2025: The company holds 1,183 BTC.

As of February 28, 2026: Holdings increased to 2,118 BTC

Today's additional purchase of 65 BTC brings the company's total holdings to 2,183 BTC

DDC Founder, Chairman, and CEO Norma Chu stated, "We are proud to have closed 2025 with record revenue and positive adjusted EBITDA, demonstrating the steady growth of the company's consumer food business and the ongoing improvement in profitability. We are building a disciplined, growth-oriented food platform and strategically allocating capital to Bitcoin assets with a long-term view, aligning with our core beliefs. We believe that this dual-track model of 'Steady Consumer Business + Strategic Bitcoin Reserve' will help DDC create lasting long-term value for shareholders."

For the full year 2025, the company defines "Adjusted EBITDA" (a non-GAAP financial measure) as: Net income / (loss) excluding the following items:· Interest expense· Taxes· Foreign exchange gains/losses· Long-lived asset impairment· Depreciation and amortization· Non-cash fair value changes related to financial instruments (including Bitcoin holdings)· Stock-based compensation

DDC Enterprise Limited (NYSE: DDC) is actively implementing its corporate Bitcoin Treasury strategy while continuing to strengthen its position as a leading global Asian food platform.

The company has established Bitcoin as a core reserve asset and is executing a prudent, long-oriented accumulation strategy. While expanding its portfolio of food brands, DDC is gradually becoming one of the public company pioneers in integrating Bitcoin into its corporate financial architecture.

Uncovering YZi Labs 229 Investment: Over 18% of the portfolio is already inactive, with an average project transparency score of 78

The business of crypto VC is becoming promising

China's AI Compute Power Counterstrike

Global Assets Plunge: Hormuz, Chips, and a South Korean Holiday

Bloomberg has reported twice, Hyperliquid once again in Wall Street's radar

Trump Backs Crypto Bill, SEC Halts Leveraged ETF, What Is the English-Speaking Crypto Community Talking About?

OpenClaw Floods Into Polymarket, Some Making Tens of Thousands Per Month

Understanding Trump's "Warfare Playbook": Ten Signals Investors Must Know

Iranian Missile Heading Toward UAE, Claude Also Within Range

Successive Core Team "Heroes" Depart, Has Aave's DAO Dream Crumbled?

Is This the Year of the Robot? A Deep Dive into Robotics Projects

When AI Takes Over Money: Bitcoin Becomes the "First Choice," Fiat Is Left Out

AI Trading in Live Markets: 4 Lessons From a WEEX Hackathon Top 10 Finalist

AI trading meets real markets. Explore 4 lessons from a WEEX Hackathon Top 10 finalist on surviving volatility, trusting AI models, and building smarter crypto trading systems.

MegaETH Co-founder: 48 Hours After Leaving Dubai, I Reassessed the Entire Crypto Space

AI within artillery range

“The cloud” is a metaphor, but the data center isn’t.

March 4th Market Key Intelligence, How Much Did You Miss?

Taking Stock of Crypto's Washington Power Players: Who is Advocating for US Crypto Regulation?

DDC Enterprise Limited Announces 2025 Unaudited Preliminary Financial Performance: Record Revenue Achieved, Bitcoin Treasury Grows to 2183 Coins

On March 4, 2026, DDC Enterprise Limited (NYSE American: DDC) today announced preliminary, unaudited full-year financial performance for the year ended December 31, 2025. The company expects to achieve record revenue and record positive adjusted EBITDA, primarily driven by continued growth in its core consumer food business and overall margin improvement. The final audited financial report is expected to be released in mid-April 2026.

Revenue: Expected to be between $39 million and $41 million, reaching a new company high.

Organic Growth: Excluding the impact of the company's strategic contraction of its U.S. operations, core revenue is expected to grow 11% to 17% year over year.

Gross Profit Margin: Expected to be between 28% and 30%, reflecting continued operational efficiency improvements.

Adjusted EBITDA: The company expects to achieve a positive full-year result in 2025, a significant improvement from a $3.5 million loss in 2024, mainly due to rigorous cost controls and a higher-margin sales mix.

In 2025, DDC's core consumer food business maintained strong operational performance.

The company also disclosed Core Consumer Food Business Adjusted EBITDA, a metric that further excludes costs related to its Bitcoin reserve strategy and non-cash fair value adjustments related to its Bitcoin holdings from adjusted EBITDA to more accurately reflect the core business performance.

In 2025, Core Consumer Food Business Adjusted EBITDA is expected to be between $5.5 million and $6 million.

In the first half of 2025, DDC initiated a long-term Bitcoin accumulation strategy, holding Bitcoin as its primary reserve asset.

As of December 31, 2025: The company holds 1,183 BTC.

As of February 28, 2026: Holdings increased to 2,118 BTC

Today's additional purchase of 65 BTC brings the company's total holdings to 2,183 BTC

DDC Founder, Chairman, and CEO Norma Chu stated, "We are proud to have closed 2025 with record revenue and positive adjusted EBITDA, demonstrating the steady growth of the company's consumer food business and the ongoing improvement in profitability. We are building a disciplined, growth-oriented food platform and strategically allocating capital to Bitcoin assets with a long-term view, aligning with our core beliefs. We believe that this dual-track model of 'Steady Consumer Business + Strategic Bitcoin Reserve' will help DDC create lasting long-term value for shareholders."

For the full year 2025, the company defines "Adjusted EBITDA" (a non-GAAP financial measure) as: Net income / (loss) excluding the following items:· Interest expense· Taxes· Foreign exchange gains/losses· Long-lived asset impairment· Depreciation and amortization· Non-cash fair value changes related to financial instruments (including Bitcoin holdings)· Stock-based compensation

DDC Enterprise Limited (NYSE: DDC) is actively implementing its corporate Bitcoin Treasury strategy while continuing to strengthen its position as a leading global Asian food platform.

The company has established Bitcoin as a core reserve asset and is executing a prudent, long-oriented accumulation strategy. While expanding its portfolio of food brands, DDC is gradually becoming one of the public company pioneers in integrating Bitcoin into its corporate financial architecture.