The Chip Industry's Most Secure Middleman Just Took a Very Risky Turn

Between $40 billion and $150 billion is not a growth curve, but a self-disruption of a business model.

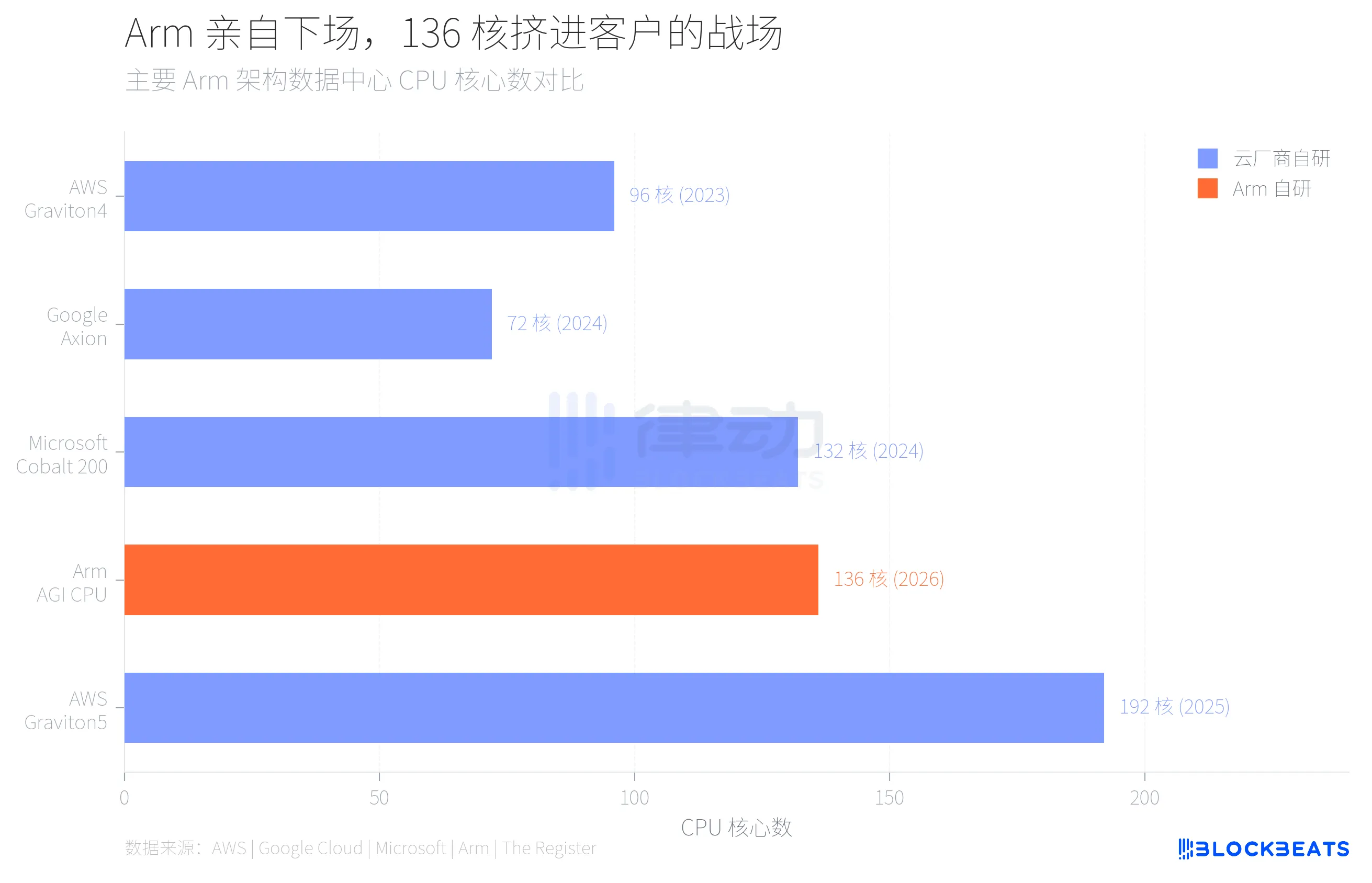

On March 24, Arm unveiled its first in-house data center CPU in the company's 35-year history in San Francisco. This chip, named AGI CPU, features 136 Neoverse V3 cores, TSMC 3nm process, 300W TDP, with Meta as the first customer for large-scale deployment within the year. Also announced as partners are OpenAI, Cerebras, Cloudflare, SAP, and SK Telecom.

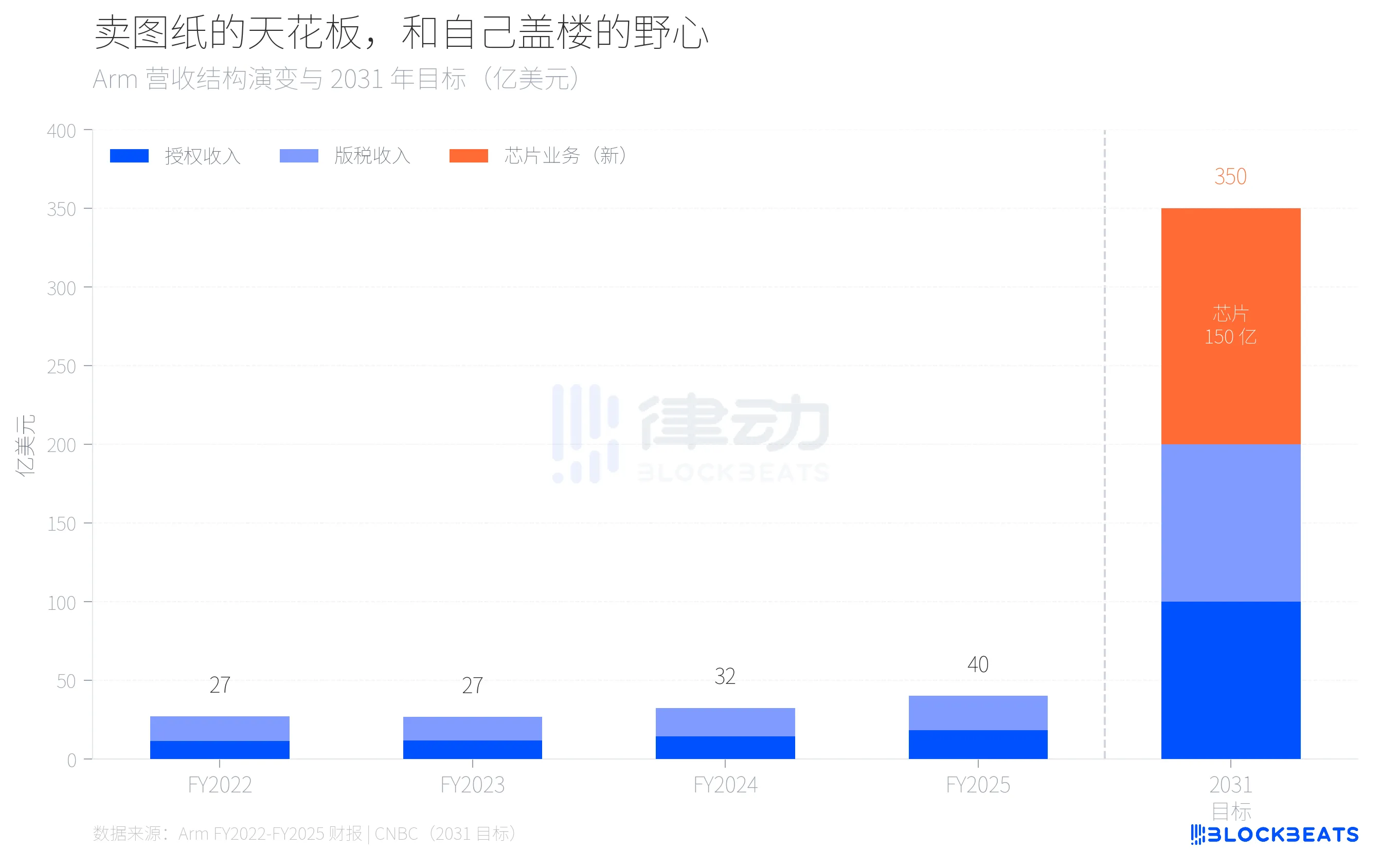

Arm CEO Rene Haas provided a set of target numbers at the event, stating that the chip business is expected to achieve $15 billion in annual revenue by 2031, with total company revenue of $25 billion and earnings per share of $9.

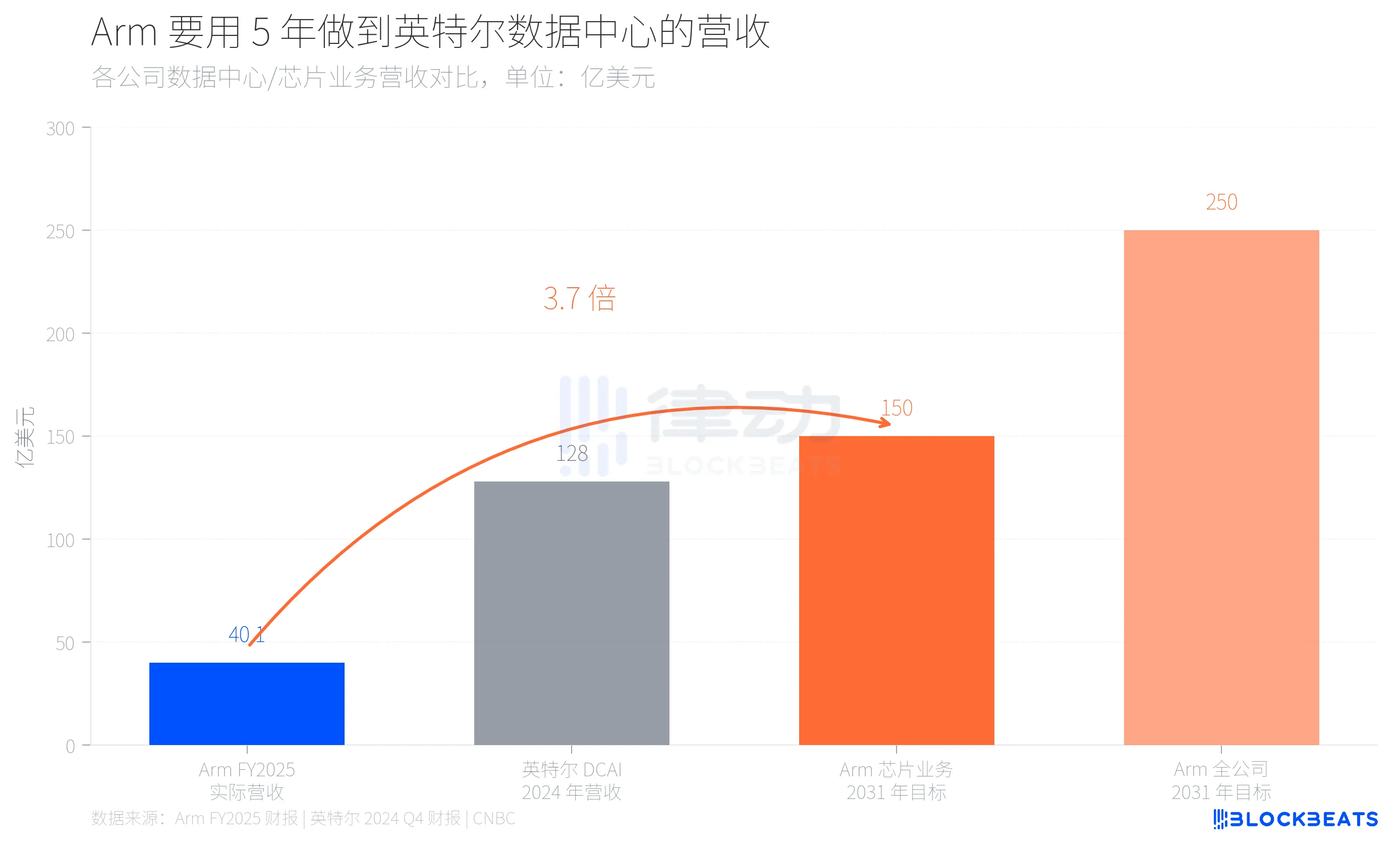

What do these numbers mean? Arm's total company revenue for FY2025 (ending March 2025) was $40.07 billion, according to Arm's annual report data, with licensing revenue of $18.39 billion, royalty revenue of $21.68 billion, and a 97% gross margin. In other words, a company with $40 billion in annual revenue aims to achieve a scale close to Intel's entire data center division in just 5 years through a single new business. According to Intel's Q4 2024 financial report, Intel's DCAI (Data Center and AI) division had full-year revenue of $12.8 billion in 2024.

From $40 billion to $150 billion, behind the 3.7x leap is Arm's attempt to transform from a pure IP licensing company to a hybrid that sells both design blueprints and finished products. There is no precedent for this in the chip industry.

Why is Arm taking this risk? The answer lies in its customer list.

Over the past three years, Arm's largest data center customers have been doing the same thing. According to public data from AWS, Amazon has migrated over 50% of EC2 compute to its in-house Graviton chips, with the latest Graviton5 featuring 192 cores. As disclosed by Google Cloud, Google's Axion chip has already migrated over 30,000 internal applications, achieving an 80% energy efficiency gain. Microsoft's Cobalt 200 is also based on Arm Neoverse architecture, TSMC 3nm process, with 132 cores.

These cloud providers all use Arm's architecture license, but the chips are self-designed, self-fabricated, and self-deployed. Arm earns licensing fees and royalties rather than chip profits. As more and more computing power is consumed by these custom chips, Arm's revenue ceiling in data centers becomes clearer.

Looking at Arm's revenue structure over the past four years, the outline of this ceiling becomes more defined. According to Arm's annual reports, from FY2022 to FY2025, the company's total revenue is projected to grow from $27 billion to $40 billion, with a CAGR of around 14%. Royalty revenue is expected to increase from $15.62 billion to $21.68 billion, while licensing revenue is set to grow from $11.41 billion to $18.39 billion. The growth rate of royalties has slowed to 20% from previous years, and this 20% growth is largely driven by the upgrade to the Armv9 architecture in the mobile sector, not in data centers.

Extrapolating this growth rate, even if both licensing and royalty revenues maintain an annual growth rate of around 20%, by 2031, they will only reach about $10 billion. The remaining $15 billion must come from a business that does not yet exist today. This is the arithmetic logic behind Arm's decision to manufacture its own chips.

Arm's choice to produce its own chips fundamentally means competing with its own customers. A company that sells blueprints to others is now constructing buildings itself, while its blueprint buyers have been building for years.

This is the true background of the 136-core AGI CPU. According to The Register, this chip has a base frequency of 3.2 GHz, up to 3.7 GHz, 12-channel DDR5 memory, 6 GB/s per core bandwidth, 96 PCIe 6.0 lanes, and supports CXL 3.0. Arm positions it as the "computing foundation of the agentic AI cloud era," focusing on CPU-side task scheduling and data flow management in AI inference, rather than directly competing with GPUs.

The pace of market share change also speaks volumes. According to Omdia's estimates, by 2025, Arm architecture servers will account for approximately 21% of global shipments, with a 70% growth rate. However, within hyperscale data centers, this proportion is already close to 50%. The 40-year dominance of x86 is not collapsing but being replaced chip by chip.

The risk of Arm's in-house chip is not technical, but relational. Meta's willingness to be the first customer is partly because Meta itself does not have a mature in-house chip project like Amazon or Google. But how would Amazon, Google, or Microsoft view this? If a supplier starts competing with you, would you still hand over your most critical architecture to them?

Arm's bet is that the overall growth of the data center is faster than the deterioration of customer relationships. Rene Haas apparently believes that the incremental demand for CPUs in the AI era is large enough to allow for both in-house chips and architecture licensing to coexist. The $15 billion target is the pricing of this assessment.

After 35 years of selling blueprints, building their own building for the first time. While they continue to sell blueprints, they are also constructing the building, all on the same plot of land. It remains to be seen whether it will be too crowded.

You may also like

The large models in the United States are moving towards closure in the name of security

Morning Report | CoinEx becomes a key hub for Iran to evade sanctions, involving over $3.8 billion in funds; Kalshi seeks a new round of financing, with a valuation potentially rising to $40 billion

From the white-haired stock god to the billionaire fund mogul, the smart people shorting Nvidia are all getting rich using the same framework

Why do cryptocurrency projects always like to change their names?

Global Launch: As predictions become the most scarce asset in the AI era, Manadia is defining the next generation of the value internet

Who is footing the bill for the $64 billion accounting frenzy?

I never expected that the first application of AI x Crypto would be in security auditing

What is your view on Binance's competitive advantages?

ETH has entered a non-consensus phase, and the turning point is approaching!

The shift in the cloud of the air: from despising stablecoins a year ago to the high-profile entry of capital today

The survival dilemma of small and medium exchanges behind the withdrawal anomalies exposed by AscendEX

Why Is Bitcoin Falling Below $60K? 5 Key Market Drivers Explained

Bitcoin has dropped sharply amid ETF outflows, Strategy stock weakness, AI stock rallies, and changing Fed expectations. Explore the key forces driving BTC’s latest correction and what traders should watch next.

Bitcoin vs. Gold in 2026: Which Asset Performs Better in Different Markets?

Morning News | The draft amendment to the People's Bank of China Law aims to clarify the legal status of digital renminbi; South Korea will transfer about 40 unregistered virtual asset service providers to law enforcement agencies

The cryptocurrency industry has entered the "Show Me" era: merely relying on vision is no longer enough

Interpreting the Ethereum Foundation's new structure: Reaffirming self-sovereignty amid institutional trends

Former SpaceX engineer reconstructs the financial execution system using first principles